Role

Lead Product Designer

Duration

8 months

Team

Product, Engineering, Compliance, Legal

Outcome

Pix approval by BACEN · IP license extended to CPF

Strategic Context

The Stakes Were Bigger Than Pix

Transfero has operated digital payment infrastructure in Brazil since its early days — including Pix for legal entities (CNPJ). But as Brazil's crypto market matured and regulation expanded, so did the scope of what compliance meant. The Banco Central do Brasil, a technological pioneer in this space, made one thing clear: operating crypto in a regulated way required meeting the same standards as any payment institution.

The inflection point was the SPSAV license — Sociedade de Pagamento e Serviços de Ativos Virtuais. Pursuing it meant shifting from a B2B model to B2B2C: individual customers, CPF accounts, retail-scale transactions. That shift changed everything. Pix for legal entities was already in place. But full Pix compliance — covering individual users, all 22 regulatory chapters, all edge cases — wasn't.

There was a prerequisite: BACEN required full Pix compliance before the SPSAV approval could move forward. Pix wasn't a feature. It was the gate.

This wasn't greenfield work. It was scope expansion under regulatory pressure — rethinking an existing payment architecture to serve a new category of user, on a deadline set by a central bank.

This wasn't my first encounter with this regulatory layer. At Clara, I had designed a digital account alongside a Payment Institution license — and deliberately deferred Pix to Phase 2, because the nominal account infrastructure had to exist first. At Transfero, I was now on the other side of that deferral: extending a B2B payment system into a fully compliant B2B2C product. Brazil's payment stack had matured. So had the design challenge. See the Clara case →

The Regulatory Challenge

22 Chapters of Mandatory UX

BACEN publishes Requisitos Mínimos para Experiência do Usuário — a 22-chapter document that specifies not just what Pix must do, but how it must behave from the user's perspective. Error messages, notification timing, key management flows, QR code generation steps, refund visibility: all prescribed in regulatory language.

Working alongside the product team, I went through every chapter to identify which requirements applied to Transfero's context — mobile-first, B2C, no physical infrastructure — and which could be deferred. The output was a clear Phase 1 scope: 13 mandatory journeys to design, build, and submit to BACEN as evidence of compliance.

Phase 1 — Delivered

- Pix with Key

- Manual Entry Pix

- Static QR Code — generation and payment

- Transaction Extract

- Refunds

- Key Management

- Pix Limits

- Scheduled Pix

- Copy-Paste Pix

- Automatic Pix

- Notifications & General Compliance

- Self-Service MED

Deferred — with documented rationale

- Dynamic QR Code backend complexity

- PSI / Payment Initiation not required for SPSAV approval

- Contact List Integration UX enhancement, non-blocking

- Internet Banking product is mobile-first

- Pix Accessibility dedicated track

Design Process

Translating Legal into Interaction

Regulatory documents are written for auditors, not designers. My work was translation: taking each obligation and converting it into a UI decision grounded in how people actually behave under uncertainty with financial flows.

Three tensions defined every design decision:

- Regulatory completeness vs. cognitive load. BACEN mandates confirmation screens, specific error states, and explicit notification requirements. The risk is turning every flow into a checklist that users stop reading. I used progressive disclosure — surfacing regulatory content at the moment it's relevant, not all upfront.

- Prevention over recovery. In regulated financial flows, a failed transaction has real consequences — for the user and for the audit trail. I prioritized validation logic early in the flow: Pix key format checks, available balance shown before the user enters any amount, limit warnings before submission.

- Mandatory must feel native. BACEN prescribes specific language for certain states — MED alerts, fraud key blocks, scheduled Pix confirmations, refund timelines. The design challenge was absorbing that language into Transfero's voice and visual system so it read as product, not as legal disclaimer bolted on.

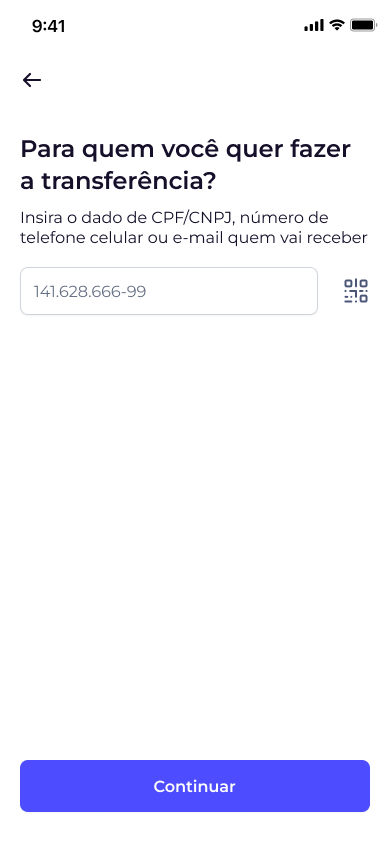

Flow — Pix with Key

The Core Journey

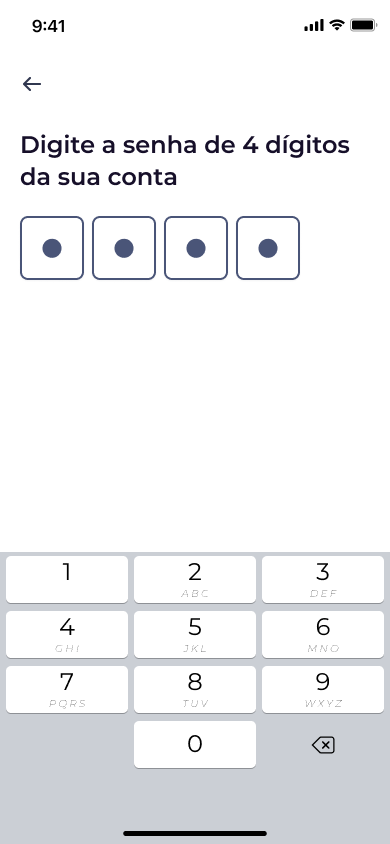

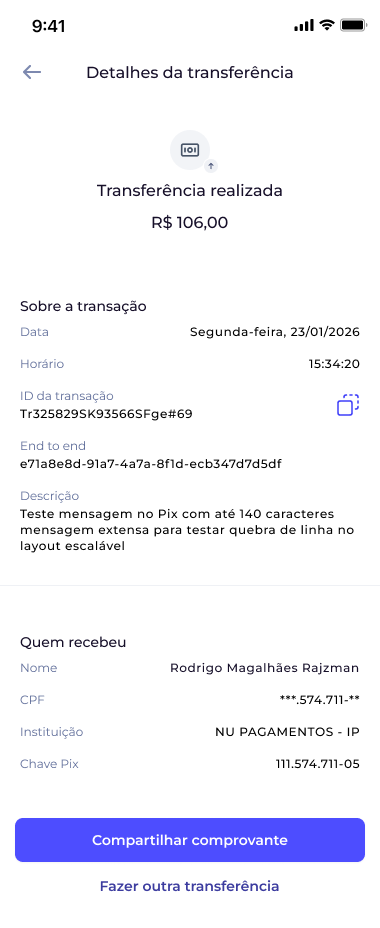

Pix with Key is the primary transfer flow — the one most users interact with daily. Every step has a direct regulatory counterpart: the confirmation review screen, the End-to-end ID in the receipt, the fraud key blocking, the authentication gate before submission.

Prevention

Available balance is shown on the amount screen before the user types anything — not as an error after the fact.

Audit trail

End-to-end ID is surfaced prominently on the receipt — BACEN mandatory, designed to feel useful rather than technical noise.

Fraud blocking

"Chave bloqueada" alert appears at review, not at submission — stopping fraud-flagged transfers before they reach authentication.

Smart input

MAX shortcut and clipboard detection (Pix Copia e Cola) reduce manual entry errors without adding flow steps.

Submission & Evidence

Design as Regulatory Evidence

For BACEN's formal review, each of the 13 journeys required documented evidence: the regulatory obligation described, the design implementation explained, and Figma screen references attached. I produced this documentation in close collaboration with the product and legal teams — the Figma files weren't just handoff artifacts, they were legal evidence.

This meant every design decision had to be traceable to its regulatory source. Screens without a documented justification couldn't make it into the submission. The discipline enforced by the regulatory process became a design quality practice: nothing arbitrary, nothing undocumented.

Outcome

Approved. And Then Some.

13

Pix journeys approved

22

Regulation chapters mapped

0

UX rework requests

8 mo

Brief to BACEN approval

BACEN approved Transfero as a Pix-compliant institution. The 13 journeys passed compliance review without rework on the UX side — a direct result of treating the regulatory document as the product spec from day one, rather than a constraint to negotiate around at the end.

More significantly: the approval unlocked the next phase of the SPSAV process. BACEN authorized the expansion of Transfero's IP license to Personal Customers (CPF), enabling transactional accounts and direct Pix access for individual users — the core capability the SPSAV licensing is built around.

The design system components produced for Pix — the review screens, authentication patterns, status vocabulary, and error states — were incorporated into BaaSiC, Transfero's broader Banking as a Service platform. I continue to work on the SPSAV project, designing the flows that the Pix certification made possible.

Prototype

Explore the Full Flows

Interactive prototype with all 13 Pix journeys — open in Figma for full navigation.